Usual Answers To Home Mortgage Questions

Authored by-Finley DempseyAre you a mortgage loan veteran? The market for mortgages is always in flux, and it can be hard to keep track of all of these changes. If you want to get the best terms on your mortgage, understanding all the changes is essential. Continue reading to gain some valuable information.

There are loans available for first time home buyers. These loans usually do not require a lot of money down and often have lower interest rates than standard mortgages. Most first time home buyer loans are guaranteed by the government; thus, there is more paperwork needed than standard mortgage applications.

Before applying for a mortgage loan, check your credit score and credit history. Any lender you visit will do this, and by checking on your credit before applying you can see the same information they will see. https://www.businesswire.com/news/home/20211130005914/en/Changes-to-the-UBS-Group-Executive-Board can then take the time to clean up any credit problems that might keep you from getting a loan.

Regardless of how much of a loan you're pre-approved for, know how much you can afford to spend on a home. Write out your budget. Include all your known expenses and leave a little extra for unforeseeable expenses that may pop up. Do not buy a more expensive home than you can afford.

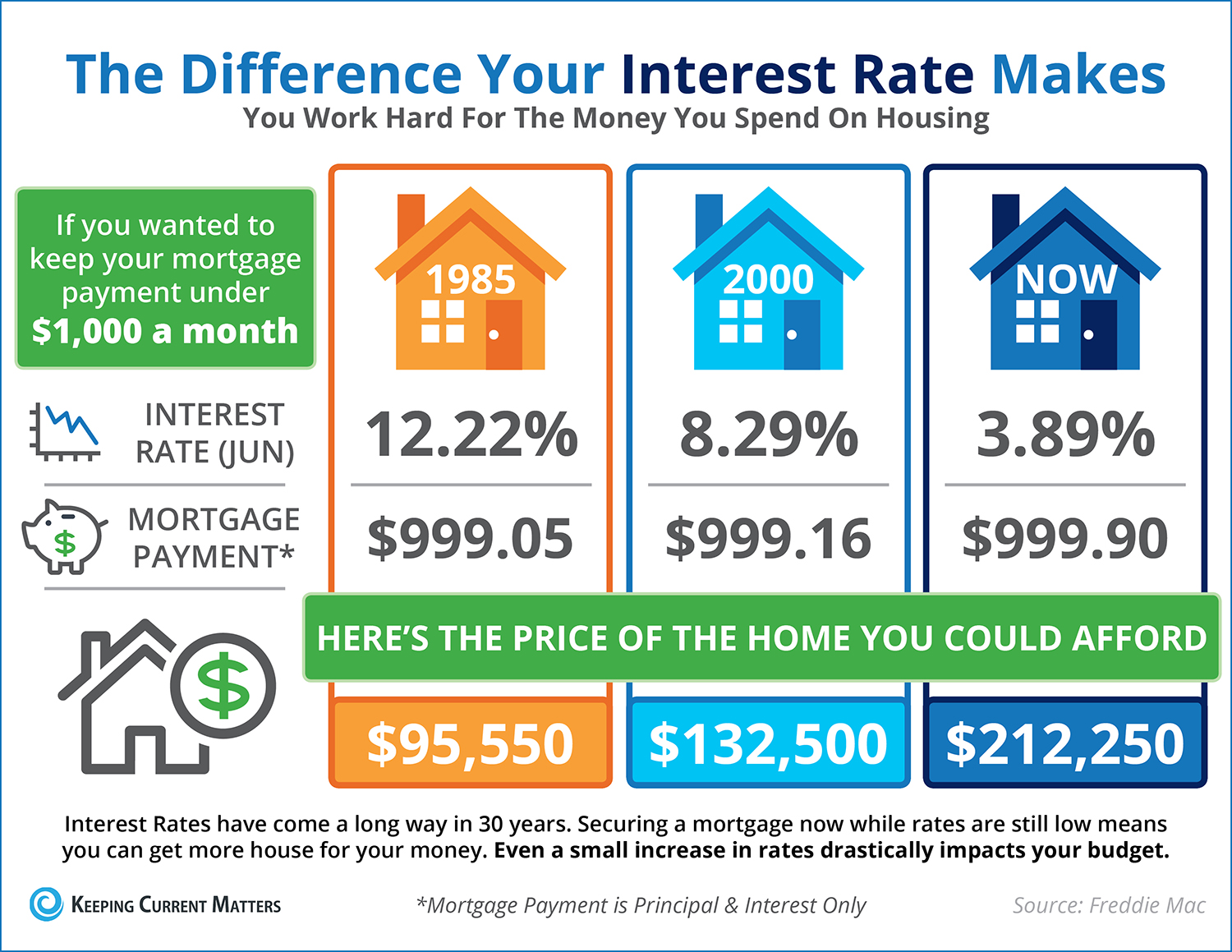

Your mortgage payment should not be more than thirty percent of what you make. Paying a lot because you make enough money can make problems occur later on if you were to have any financial problems. Manageable payments are good for your budget.

Try getting pre-approved for a mortgage before you start looking at houses. This will make the closing process a lot easier and you will have an advantage over other buyers who still have to go through the mortgage application process. Besides, being pre-approved will give you an idea of what kind of home you can afford.

Consider a mortgage broker instead of a bank, especially if you have less than perfect credit. Unlike banks, mortgage brokers have a variety of sources in which to get your loan approved. Additionally, many times mortgage brokers can get you a better interest rate than you can receive from a traditional bank.

Make sure that all of your loans and other payments are up to date before you apply for a mortgage. Every delinquency you have is going to impact your credit score, so it is best to pay things off and have a solid payment history before you contact any lenders.

Check with your local Better Business Bureau before giving personal information to any lender. Unfortunately, there are predatory lenders out there that are only out to steal your identity. By checking with your BBB, you can ensure that you are only giving your information to a legitimate home mortgage lender.

Use local lenders. If you are using a mortgage broker, it is common to get quotes from lenders who are out of state. Estimates given by brokers who are not local may not be aware of costs that local lenders know about because they are familiar with local laws. This can lead to incorrect estimates.

Keep your job. Lenders look into many aspects of your financial situation and one very important aspect is your employment income. Stability is very important to lenders. Avoid moving jobs or relocating for as long as possible before you apply for a home mortgage. This will show them that you are stable.

Keep your credit score in good shape by always paying your bills on time. Avoid negative reporting on your score by staying current on all your obligations, even your utility bills. Do take out credit cards at department stores even though you get a discount. You can build a good credit rating by using cards and paying them off every month.

Compare multiple factors as you shop for a mortgage. Clearly, you are interested in finding a low interest rate. In addition, you need to evaluate all types of mortgage products. Closing costs, down payment requirements, and other costs involved in home buying need to be considered, too.

Ask your lender in advance what documentation they need before you meet with them. https://bankingjournal.aba.com/2021/12/kentucky-tornadoes-ag-banks-provide-more-than-financial-resources/ is usually going to include tax returns, income statements and W2s, although more might be needed. The more time you have to get it all together is the less likely you'll be unprepared at the actual meeting time.

When rates are near the the bottom, you should consider buying a home. If you do not think that you will qualify for a mortgage, you should at least try. Having your own home is one of the best investments that you can make. Quit throwing away money into rent and try to get a mortgage and own your own home.

Talk to the BBB before making your final decision. Deceitful brokers may con you into paying high fees and refinancing so that they can make more money. If a broker wants you to pay excessive points or high fees, be cautious.

Be prompt about getting your documentation to your lender once you have applied for a home mortgage. If your lender does not have all the necessary documentation on hand, and you have begun negotiations on a home, you could end up losing lots of money. Remember that there are nonrefundable deposits and fees involved, so you must get all your documentation submitted in a timely manner.

Do not do anything that will raise red flags to the lender while you are waiting for approval. Co-signing on a loan for someone else, changing jobs, moving to a new address or applying for a name change are all things that should never be done until after your loan is closed.

Realizing that you have just bought a home and have a good mortgage is a great feeling. This is a loan that you're going to carry for years, and you want it to be both affordable and accommodating. So, use the information that has been passed on to you so that you can find a good mortgage.